Maximize Cost Benefits with USDA loan refinance Tailored to Your Requirements.

Maximize Cost Benefits with USDA loan refinance Tailored to Your Requirements.

Blog Article

Maximize Your Financial Liberty: Benefits of Car Loan Refinance Explained

Car loan refinancing offers a tactical possibility for individuals seeking to boost their financial flexibility. By safeguarding a lower rate of interest price or changing finance terms, debtors can successfully minimize monthly payments and boost cash flow.

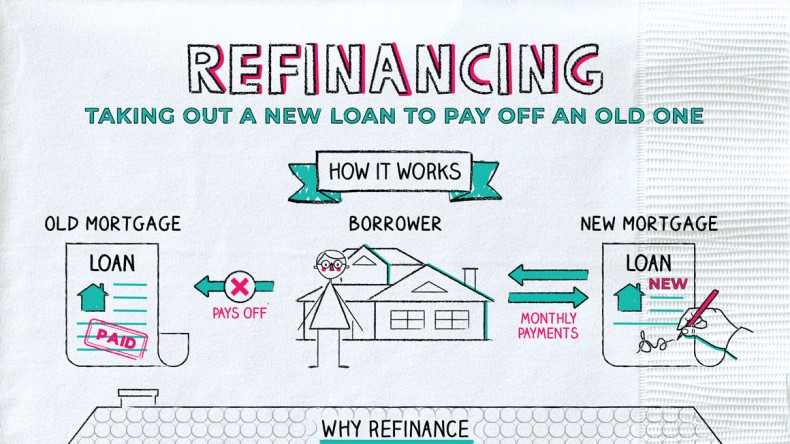

Recognizing Lending Refinancing

Comprehending loan refinancing is important for property owners seeking to maximize their monetary situation. Lending refinancing entails changing an existing mortgage with a new one, normally to attain better car loan terms or problems. This monetary approach can be used for various reasons, including changing the funding's period, modifying the sort of rate of interest, or combining financial debt.

The main objective of refinancing is usually to decrease regular monthly repayments, thereby improving cash flow. Homeowners might also refinance to access home equity, which can be utilized for significant expenses such as home renovations or education. Additionally, refinancing can offer the possibility to switch from an adjustable-rate home loan (ARM) to a fixed-rate home loan, offering even more stability in regular monthly repayments.

Nonetheless, it is important for homeowners to review their financial circumstances and the associated prices of refinancing, such as shutting expenses and fees. A comprehensive analysis can aid figure out whether refinancing is a prudent decision, stabilizing prospective cost savings against the first costs involved. Eventually, recognizing car loan refinancing equips house owners to make enlightened decisions, enhancing their economic wellness and leading the way for long-term security.

Reducing Your Rates Of Interest

Lots of homeowners look for to reduce their rate of interest as a primary motivation for re-financing their mortgages. Decreasing the rate of interest price can considerably reduce month-to-month payments and total borrowing prices, allowing people to assign funds in the direction of other economic goals. When rate of interest rates decline, re-financing provides a possibility to secure an extra beneficial financing term, eventually boosting financial security.

Refinancing can result in considerable financial savings over the life of the loan (USDA loan refinance). Minimizing a rate of interest price from 4% to 3% on a $300,000 home mortgage can result in thousands of dollars saved in interest payments over 30 years. Additionally, lower rates may enable homeowners to pay off their loans extra rapidly, thus enhancing equity and decreasing financial obligation faster

It is important for property owners to assess their current mortgage terms and market problems prior to making a decision to refinance. Assessing potential savings versus re-financing expenses, such as closing fees, is crucial for making an educated choice. By taking advantage of lower rates of interest, house owners can not just boost their financial freedom yet likewise create a more safe and secure financial future for themselves and their families.

Settling Financial Obligation Efficiently

Property owners commonly find themselves handling several debts, such as charge card, individual fundings, and other economic responsibilities, which can result in increased anxiety and challenging monthly settlements (USDA loan refinance). Consolidating financial obligation properly via loan refinancing uses a structured remedy to manage these monetary burdens

By re-financing existing financings right into a solitary, more workable lending, home owners can simplify their payment procedure. This technique not just lowers the number of regular monthly settlements but can likewise decrease the overall rate of interest rate, relying on market problems and specific credit rating accounts. By settling debt, house owners can allot their resources much more effectively, maximizing cash circulation for essential expenses or cost savings.

Readjusting Funding Terms

Changing financing terms can significantly affect a house owner's economic landscape, especially after consolidating existing financial obligations. When re-financing a home mortgage, consumers can modify the length of try this out the lending, rate of interest prices, and payment timetables, straightening them extra very closely with their existing economic scenario and goals.

For instance, extending the lending term can lower monthly payments, making it less complicated to handle capital. However, this may result in paying even more passion over the life of the loan. Alternatively, selecting a much shorter lending term can lead to higher month-to-month settlements however substantially minimize the total interest paid, permitting consumers to develop equity more promptly.

In addition, changing the rate of interest can affect general affordability. Homeowners might change from an adjustable-rate home loan (ARM) to a fixed-rate home loan for security, securing in reduced rates, particularly great post to read in a positive market. Re-financing to an ARM can supply lower preliminary settlements, which can be helpful for those expecting a rise in earnings or economic scenarios.

Improving Money Flow

Re-financing a home loan can be a strategic strategy to enhancing cash circulation, enabling borrowers to allot their financial resources better. By protecting a lower rates of interest or expanding the funding term, property owners can significantly minimize their monthly home mortgage payments. This immediate reduction in expenses can release up funds for other necessary needs, such as settling high-interest debt, saving for emergency situations, or investing in possibilities that can generate higher returns.

Additionally, refinancing can provide debtors with the option to convert from an adjustable-rate home mortgage (ARM) to a fixed-rate home loan. This change can stabilize regular monthly settlements, making budgeting less complicated and improving monetary predictability.

An additional avenue for enhancing capital is with cash-out refinancing, where house owners can obtain against their equity to gain access pop over to this site to fluid funds. These funds can be used for home renovations, which might enhance building value and, consequently, money circulation when the home is sold.

Conclusion

In conclusion, loan refinancing presents a critical possibility to boost monetary flexibility. By reducing interest rates, consolidating financial obligation, adjusting loan terms, and boosting cash money circulation, individuals can achieve an extra desirable monetary setting.

Report this page